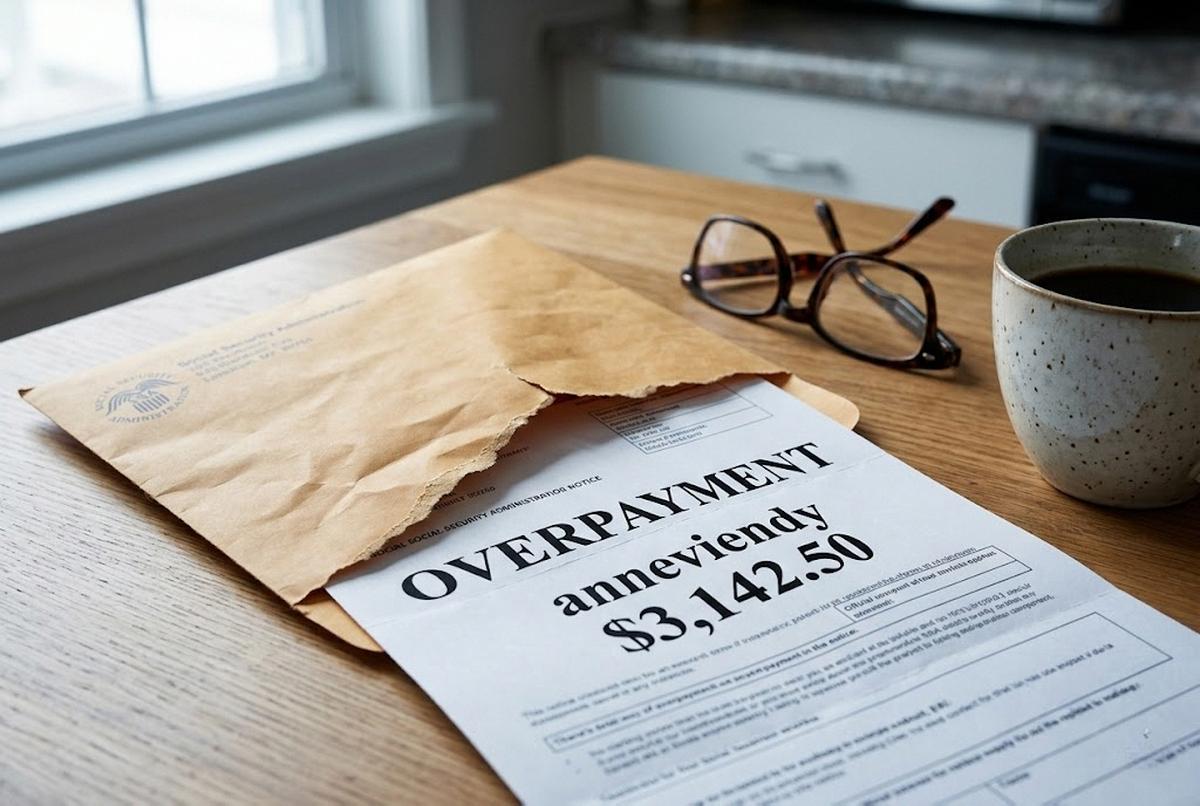

Roberta Hollings was sixty-eight, three years widowed, and standing at her mailbox on a Tuesday in March when she opened the envelope from the Social Security Administration. The letter said she had been overpaid $14,247 in survivor benefits going back to 2022. It said she had thirty days to respond. It said that if she did nothing, SSA would begin withholding 50% of her monthly check starting in May.

Roberta called me from her kitchen in Norwalk that afternoon. She kept saying the same sentence: "I didn't do anything wrong." Her voice was steady but her hands weren't — I could hear the paper rattling against the phone. She had not done anything wrong, as it turned out. SSA had miscalculated her late husband's earnings record and taken three years to notice. None of that mattered to the form letter. What mattered was the 30-day clock.

If you've gotten one of these letters — or you're afraid you might — this is what I want you to know. Pay attention to that clock. It's the most important number on the page.

The Clawback Rule Changed in 2025, and Most People Still Haven't Heard

From March 2024 to April 2025, under Acting Commissioner Martin O'Malley, SSA temporarily capped overpayment recovery at 10% of your monthly check. That cap was reversed in April 2025. Any overpayment notice issued after April 25, 2025 is now subject to a 50% withholding rate. The agency calls this the "default rate." I call it a financial earthquake for anyone living on a fixed income. The new rule arrived alongside the broader 2026 Social Security changes most retirees never read past the first page of.

The scope is staggering. According to SSA's own data, roughly one million beneficiaries currently owe a collective $23 billion in overpayments. Some of these debts go back a decade or more. SSA didn't catch them. The beneficiary didn't know about them. And now — after a policy reversal that got almost no mainstream coverage — the agency is allowed to take half your check until the balance is gone.

A client of mine in Stamford, retired UPS dispatcher, gets $2,184 a month. If SSA decided he'd been overpaid $9,000, his check would drop to $1,092 starting on the first applicable payment date. For roughly eight months. He had no idea this was even possible until I walked him through it at a Westport Senior Center workshop last fall. Half the room didn't know either.

This is not a small administrative correction. This is the difference between paying your property taxes and not paying them.

What an Overpayment Notice Actually Looks Like

The letter usually arrives in a window envelope. The header says "Notice of Overpayment." Toward the top, there's a dollar figure — the total amount SSA claims you owe. Below that, a paragraph or two explaining why, often in language so vague it's nearly useless: "Our records show you received benefits to which you were not entitled."

Further down, on page two or three, you'll find the part that matters most. There's a section that explains your rights. It will mention three options: pay in full within 30 days, request a waiver using Form SSA-632-BK, or request reconsideration using Form SSA-561-U2. It will also tell you that if you do nothing, withholding begins on a specified date — usually about 60 days out.

Read the whole letter. Twice. Then look at the date stamp. Your 30-day clock starts the day SSA mailed the notice, not the day you opened it. If the letter sat in your mail pile for a week because you were visiting your daughter in Phoenix, you've already lost a week.

The 30-Day Window — Why It Matters More Than the Money

Here is the rule that almost nobody knows. A pending waiver or reconsideration request blocks collection while SSA reviews it — that part is regulation, not courtesy. The trick is timing. Collection can begin as soon as 30 days after the notice date (your letter names the exact date, often around 60 days out). File Form SSA-632-BK (a waiver) or Form SSA-561-U2 (reconsideration) inside that 30-day window and the withholding never starts. One important thing about the waiver: it has no filing deadline. You can request a waiver at any time — even months later — and a pending waiver still pauses collection, though if you wait past the 30 days the agency may have already started taking money before it stops. Reconsideration does have a deadline: 60 days from the notice to count as a timely appeal.

Miss the window, and the 50% withholding starts on schedule. You can still file the forms after the deadline, and SSA may still grant relief, but the money starts coming out of your check in the meantime. For someone living check to check, that gap can mean missed mortgage payments, skipped prescriptions, or worse.

I've watched clients lose three months of full benefits because they wanted to "think about it" before filing. Don't think about it. File first. You can always withdraw the request later if it turns out the overpayment is legitimate and you'd rather just pay it off. But you cannot retroactively pause collection.

Form SSA-632-BK: The Waiver That Wipes the Debt

The waiver is the gold standard outcome. If SSA grants it, the overpayment goes away. You owe nothing. The money you already received is yours to keep.

To qualify, you have to prove two things. First, that the overpayment was not your fault. Second, that paying it back would either cause financial hardship or be "against equity and good conscience." That second phrase is straight out of the regulations and it's surprisingly flexible.

"Without fault" generally means one of three things: you didn't know about the overpayment, you couldn't have reasonably known, or you gave SSA all the relevant information at the time and they processed it incorrectly. Roberta Hollings, the widow in Norwalk, met all three. She'd reported her husband's death. She'd submitted the forms SSA asked for. She had no way of knowing that someone in Baltimore had punched in the wrong earnings figure. We attached her original correspondence — copies of the letters she'd sent in 2022, her certified-mail receipts — to the SSA-632-BK and submitted it within nineteen days of the notice.

The financial-hardship piece is where you list everything. Monthly income, monthly expenses, savings, debts. SSA looks at whether you have enough "defensible" income left after necessary expenses to actually pay the debt back. If your monthly Social Security check is your only meaningful income and your expenses already eat most of it — which is true for a huge percentage of beneficiaries — you almost certainly qualify.

The form runs about ten pages. It looks intimidating. It is not as bad as it looks. Most of it is the income/expense worksheet. Be honest. Be specific. Use real numbers from real bills. SSA can and will ask for documentation, so back up what you write.

Form SSA-561-U2: When You Think SSA Is Just Plain Wrong

The waiver says "yes, you overpaid me, but I shouldn't have to pay it back." The reconsideration says "no, you didn't actually overpay me — your math is wrong."

File a reconsideration when you genuinely believe SSA made an error in the underlying calculation. Maybe they're double-counting earnings. Maybe they're using outdated marital-status information. Maybe they applied the wrong cost-of-living adjustment. Whatever it is, you're disputing the existence or amount of the overpayment itself, not asking for forgiveness of one you concede.

SSA-561-U2 is shorter than the waiver — about two pages. You write a clear, dated explanation of what you think they got wrong, attach any documents that support your version, and send it in. If you file within 60 days, collection pauses while they review.

Here's what I tell clients: you can file both. Send the reconsideration first, arguing the overpayment doesn't exist. If SSA still rules against you, you then file the waiver, conceding the overpayment and asking for it to be forgiven. You don't get one shot. You get the whole sequence.

The Income-Based Repayment Plan (When the Other Options Don't Apply)

Not every situation supports a waiver. Maybe you genuinely received money you weren't entitled to and you knew it at the time. Maybe the math is correct and the fault is on you. In that case, the realistic question becomes: how fast do I have to pay this back?

This is what Form SSA-634-BK exists for. It's a Request for Change in Overpayment Recovery Rate. You use it to ask SSA to lower the withholding from 50% to something you can actually afford. The form asks for the same kind of income/expense detail as the waiver. SSA reviews it and, if your numbers support it, sets a new rate — sometimes as low as $50 a month, sometimes 10% of the check, sometimes a flat dollar amount you negotiate.

I had a client who ended up paying back a legitimate $6,200 overpayment at $40 a month. It took a long time. But his check stayed whole. His mortgage stayed paid. Sometimes the goal isn't winning. Sometimes the goal is keeping the lights on.

Why These Letters Show Up in the First Place

In my experience, overpayment notices fall into a handful of recurring buckets. Knowing the pattern helps you understand what SSA is actually claiming.

The biggest one is late-reported earnings. If you're under full retirement age and still working, SSA's earnings test reduces your benefits when your wages exceed the annual threshold ($24,480 for 2026). If you didn't report a raise or a side job promptly, SSA finds out two years later when the IRS hands them your tax return. Cue the letter.

A close second is changes in living arrangements, especially for SSI recipients. Move in with an adult child, get married, get divorced, take in a roommate — any of these can change your benefit amount. If you didn't report it within ten days, SSA assumes you were overpaid for every month it took them to figure it out.

For disability beneficiaries, the Continuing Disability Review (CDR) is its own category. SSA periodically reviews whether you still qualify medically. If they decide you should have been off the rolls a year ago, every check between then and now becomes an overpayment. The same lookback logic appears in retirement-side missteps too — a missed first required minimum distribution can spike your reported income and trigger a re-evaluation of needs-based supplements. Or a Medicare IRMAA surcharge, if your MAGI crossed a threshold you didn't see coming.

And finally, the one that hurt Roberta: dual-entitlement calculation errors. When you're entitled to benefits on more than one record (your own and a spouse's, or your own and a deceased spouse's), the math gets ugly. Survivor cases are particularly error-prone — I've written separately about what happens to a spouse's Social Security when they die and the calculation traps that follow. SSA gets it wrong frequently. They catch it eventually. You get the letter.

How to Actually Reach Someone at SSA

This is the part of the article I genuinely struggled to write, because the truthful answer is that it's harder than it should be. With many SSA field offices reducing in-person hours, reaching the agency online has become its own skill. If you've already had to wait on hold to talk to anybody about your benefits, you know what I mean. AARP has been tracking the clawback issue closely and even they describe the appeals process as "opaque."

Here's what tends to work, in roughly this order.

The national line is 800-772-1213. Call between 7:30 and 8:00 a.m. Eastern, Tuesday through Friday. Mondays are brutal. Press 5, then 1, then your Social Security number. The wait can still be an hour. Bring a book.

The local field office is sometimes faster. Find yours at ssa.gov/locator. You can call directly, though many offices route to the national queue during peak hours. In-person appointments must be scheduled — walk-ins are technically possible but realistically a half-day affair. If your case is complex, ask for the Claims Specialist who handles overpayment cases at that office. There's usually one. They'll know more in five minutes than the national queue knows in fifty.

If you're getting nowhere, call your U.S. Senator's or Representative's caseworker. Every congressional office has staff whose entire job is unsticking constituent problems with federal agencies. They have direct lines into SSA. I've seen a single email from a senator's caseworker resolve a six-month-old overpayment dispute in a week. It's a legitimate channel and it's underused. Most members of Congress have an online form for casework requests on their official website.

Write this script down before you call: "My name is [name]. My Social Security number is [number]. I received an overpayment notice dated [date] for $[amount]. I am requesting a waiver of recovery using Form SSA-632. Can you confirm that filing this form pauses collection, and can you tell me where to mail or upload the completed form?"

You'll get an answer faster if you sound like you already know the rules.

What I'd Do This Week If I Got That Letter

If an overpayment notice landed in your mailbox today, here's the order of operations:

- Note the date on the letter. That's the start of your 30-day window to file before withholding can begin (the waiver itself has no hard deadline, but filing inside 30 days is what keeps your check whole) and your 60-day deadline to file a timely reconsideration. Write the dates on your calendar in pen.

- Read the entire letter twice. Find the dollar amount, the reason given, and the section that explains your rights. If anything's unclear, mark it.

- Decide which form fits your situation. SSA-561-U2 if you think the overpayment itself is wrong. SSA-632-BK if you concede the overpayment but want it forgiven. SSA-634-BK if you're not contesting it but can't afford 50% withholding. You can file more than one in sequence.

- Download the forms from ssa.gov/forms. Fill them out by hand or PDF, whichever you find easier. Don't leave fields blank — write "N/A" if it doesn't apply.

- Mail them certified, return-receipt requested. Or upload through your my Social Security account. Either way, keep proof of submission. The post office costs about $5 and is worth every penny if you ever need to prove you filed on time.

- Call SSA to confirm receipt about a week after submission. Get a name, a date, and a confirmation that collection has been paused.

- If you're being stonewalled, call your congressional caseworker. Tell them what you filed, when, and what response you've received (or haven't).

One small thing. Make a copy of every single page of every form before you send it. Keep it in a folder labeled clearly. If this drags on for months — and it sometimes does — you will be glad you did.

A Word About Why This Matters

My father Arthur, who I've written about before, was the kind of man who paid every bill the day it arrived. If a federal agency had ever sent him a letter saying he owed $14,000, his first instinct would have been to write the check. He would have assumed the government doesn't make mistakes. He would have been wrong, and it would have cost him.

SSA makes mistakes constantly. A 2024 inspector general report estimated that a meaningful share of overpayment cases involve agency error — not beneficiary fraud, not late reporting, just bureaucratic miscalculation. The 50% clawback rule treats every overpayment the same way regardless of fault. The forms exist precisely because Congress recognized that the agency would otherwise be punishing people for its own errors.

Use the forms. File on time. Don't write the check until you've exhausted the appeals. And if you're helping a parent, a neighbor, or a widowed friend who got one of these letters — sit with them at the kitchen table and walk through the deadlines together. The 30-day window saves checks. I've watched it do exactly that, more than once.

Roberta Hollings got her waiver granted in late September. SSA conceded the calculation error, wiped the debt, and sent her a small back-payment for the months they'd already taken from her check before she filed. She mailed me a thank-you card with a pressed pansy from her garden. I keep it in the same folder where I keep the Post-it that says "feel the weight."

You've handled harder paperwork than this. You can handle this too. And you don't have to do it alone.