A woman named Loretta showed up at my Westport Senior Center workshop three Aprils ago with a question she'd clearly been rehearsing. She was 64, recently retired from teaching high school biology in Bridgeport, and she stood up during the Q&A and said, "My mother is 87 and I have no idea where any of her money is. I don't know if she has a will. And every time I try to ask, she acts like I'm trying to rob her."

Nobody laughed. Half the room nodded.

In my experience, this is the most avoided conversation in American family life. Not politics. Not religion. Money. Your aging parent's money, specifically: where it is, how much exists, who gets it, and what happens when they can't manage it anymore. A 2024 Fidelity Investments survey found 57% of adult children have never discussed finances with their parents. Not once. And roughly 40% of those who tried said it went badly enough to kill any second attempt.

My father Arthur worked at Pratt & Whitney for 34 years and balanced his checkbook every Friday with a mechanical pencil. He refused to discuss his finances with me for six years. He finally cracked at Hartford Hospital at 10 PM, sitting with a broken wrist in a temporary cast after tripping at a company reunion. "Maybe we should talk about some things," he said. He was 78.

So when Loretta asked her question, I skipped the checklist and told her what I wished someone had told me.

Why This Conversation Feels Impossible

Money and control are the same thing when you're 82.

Your parent paid the mortgage, raised the kids, survived recessions. For decades, every financial decision was theirs alone. Now you're suggesting they share account passwords. Of course they're defensive.

The resistance runs deeper than stubbornness. It's fear. A retired postal supervisor in Norwalk, a man named Clifford, once told me he'd rather get a root canal than show his daughter his bank statements. "She'll see the annuity," he said. He'd been sold a variable annuity at a free dinner seminar — $14,000 surrender penalty — and he'd been hiding the shame of it for three years. While Clifford hid the annuity, he was also hiding $6,200 in unpaid property taxes and a lapsed homeowner's insurance policy. His daughter found all of it when he was hospitalized for pneumonia and she started opening his mail.

Every financial planner has a version of this story. The pattern doesn't change.

When to Start

If your parent is cognitively sharp and managing their bills without trouble, the best time is now. Not after the fall. Not after the diagnosis.

Look for what I call "gateway moments":

- A news story about Social Security changes. "Mom, did you see this?"

- A relative's health scare. "Uncle Ray's family couldn't find his documents. We should be more prepared."

- Your own planning. "Dad, Maggie and I just updated our wills. Made me realize I don't know where yours is."

Maggie suggested the third approach. She said the trick is making it mutual, not parental. She's right.

The key phrase is "us," not "you." The sentence that finally worked with Arthur: "Dad, if something happened to me tomorrow, Maggie wouldn't know where half our accounts are either. Can we both get organized?" His posture changed. He wasn't the problem anymore. We both were.

What You Actually Need to Know

You don't need your parent's net worth down to the penny. You need to know where things are and who to call. The difference matters.

Bank accounts. Which banks, which branches, approximate balances. Are there accounts at credit unions, online banks, or institutions you've never heard of? My father had a savings account at a credit union affiliated with Pratt & Whitney. None of us knew. It held $11,400, and we found it seven months after he died, purely by accident, sorting through a drawer of old pay stubs. That discovery haunts me because it was pure luck. What if the drawer had been tossed?

Income sources. Social Security amount, pensions, annuity payments. You need these numbers to plan for the gap between income and the cost of care. The gap arrives faster than anyone expects.

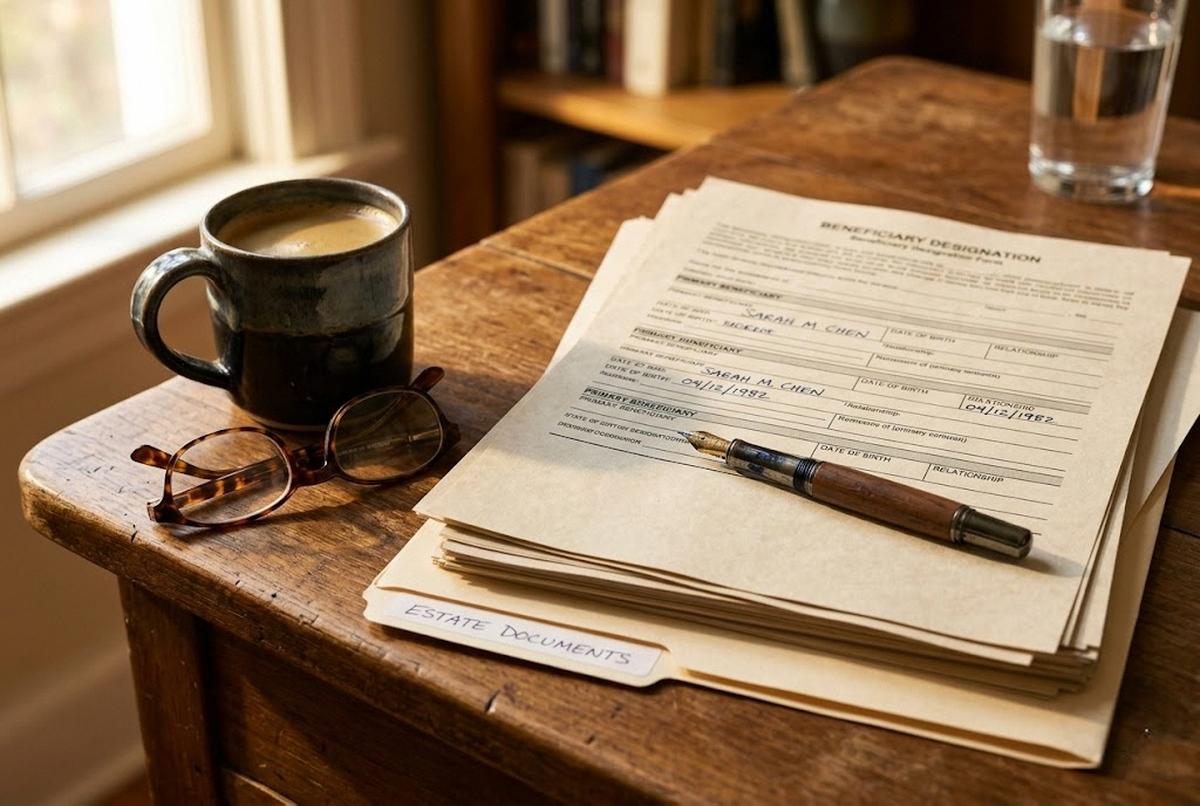

Insurance. Medicare parts and supplements, life insurance with face values and beneficiaries, long-term care insurance with the daily benefit and elimination period noted, homeowner's, auto. Check beneficiary designations carefully. Outdated ones naming a deceased spouse or an ex-son-in-law create legal headaches costing thousands. A client's wife discovered her husband's $250,000 term policy still named his first wife as beneficiary. He'd meant to change it for nine years. Nine years of meaning to.

Debts. Mortgage balance, car loans, credit cards, medical bills. Debt doesn't disappear when someone dies. Secured debt follows the asset.

Legal documents. Will or trust, power of attorney for both financial and healthcare decisions, living will or advance directive. Do they exist? Are they current? Where are the originals physically located?

Document location. If your parent uses a fireproof safe, know the combination. Safe deposit box? Know which bank and where the key is. A will locked in a box nobody can open is the same as no will at all.

Don't try to cover everything in one sitting. Spread it across two or three conversations. Write things down in front of them so they can see you're being careful with the information.

Warning Signs of Financial Decline

Sometimes the conversation isn't optional. The mail pile speaks when your parent won't.

Unopened bills. Not junk mail. Actual bills, Medicare Explanation of Benefits forms, property tax statements sitting sealed on the counter or stuffed in a kitchen drawer. When Beverly, a 79-year-old widow in Fairfield, had a mild stroke, her son found 14 weeks of unopened mail rubber-banded in a grocery bag under the hall table. Three were final notices.

Unusual purchases or donations. QVC orders arriving daily. Large checks to charities they've never mentioned. A 2023 AARP study estimated seniors lose $28.3 billion annually to financial exploitation — and much of it starts small. A $200 phone solicitation. A $49 monthly "tech support" subscription.

Trouble with basic math. Wrong tip amounts. Checks written for wrong figures. My father started writing his mortgage payment as $840 instead of $804. The bank processed it each time. Five months before anyone caught it.

Susceptibility to scams. If your parent mentions a call about their "Medicare account being suspended," stop everything. Scam tactics targeting seniors have gotten sophisticated enough to fool sharp people. Don't lecture. Say: "Those scammers are professionals. Let's report it together."

One sign might mean nothing. Three together? Act.

Power of Attorney: The $350 Document or the $10,000 Problem

A durable financial power of attorney costs $150 to $400 through an elder law attorney. Thirty minutes to sign. Your parent names a trusted person with authority to manage accounts, pay bills, and handle decisions if they become unable to.

Without one? You're petitioning the probate court for conservatorship. In Connecticut, the total runs $3,000 to $8,000. In New York, I've seen it exceed $15,000. Six weeks to four months of processing — and during the entire gap, your parent's mortgage is due, their insurance premium is due, their electric bill is due. You cannot legally write a single check on their behalf.

Back in 2014, a daughter flew in from Seattle when her father had a stroke. No POA existed. Petitioning the Stamford probate court for emergency conservatorship cost $3,400 in legal fees. Six weeks of paperwork. Her father couldn't pay his mortgage during the gap. All preventable with a document costing less than dinner for two at Acqua, the Italian place on Main Street here in Westport.

Get it done while your parent can still sign. "Can still sign" means they understand the document and can communicate their wishes. Once dementia progresses past a certain point, the window closes. It does not reopen.

How to Organize Everything

Here is my system. Same one I used for Arthur's affairs, same one I recommend to every client who sits in my office.

- Buy a three-ring binder. Physical paper. Old-fashioned, yes. But digital files vanish inside cloud accounts nobody has passwords to. A binder sits on a shelf. It can't crash.

- Tab it by category. Bank accounts. Income. Insurance. Debts. Legal documents (copies only; originals go in a safe). Monthly bills and autopay schedules. Contacts: financial advisor, attorney, accountant, doctors.

- Put a one-page summary at the front. Name, date of birth, Social Security number, Medicare number, primary bank, emergency contacts, attorney phone number. When crisis hits at 2 AM, you want one page telling you who to call.

- Update it once a year. Their birthday. Tax day. January 1st. Balances change, policies lapse, accounts get opened.

- Tell one other person where it is. A sibling. The attorney. Redundancy matters!

My colleague Eileen Brennan, an elder law attorney in Stamford, calls the binder "the gift you give your family before they need it." For the digitally inclined, a password manager like 1Password works as a supplement. But the binder comes first. Always.

When the Conversation Goes Wrong

My father didn't speak to me for two weeks after my first attempt. I'd been too clinical — too much the financial planner, not enough the son. He heard "I think you're incompetent" when what I said was "we need to discuss your finances."

Two weeks of silence from a man who lived 90 minutes away.

When he finally called, it was about UConn basketball. Geno Auriemma's recruiting class. Twenty minutes, not a word about money. The next visit, I brought Dunkin' Donuts and sat at his kitchen table and asked about his pension. He told me. Not everything, but enough.

What I learned from failing:

Don't ambush. A holiday dinner with the whole family is the worst possible setting. One-on-one works better.

Don't lead with fear. "What if you get dementia" shuts the door. "I want to make sure your wishes are followed" keeps it open.

Bring your own vulnerability. Share something about your own finances first. Parents open up when you're not playing authority figure.

Accept partial wins. Maybe they'll reveal where the will is but not how much they have in savings. Take it! Come back next month.

Try a neutral third party. Their advisor, their attorney, their pastor. The message lands differently from someone who isn't their child.

And if they flatly refuse? Document what you do know. Watch for the warning signs above. The conversation may become mandatory whether anyone is ready or not.

What I Tell My Own Kids

Sarah texted me last fall from her apartment near Yale-New Haven Hospital. Three words: "Dad, the binder."

She'd been talking to a colleague whose father died without organized records. The family spent eight months untangling accounts and paid a probate attorney $12,000 to sort what a three-ring binder could have prevented.

I texted back: "Top shelf of the study closet. Green binder. Updated last March." David, in Austin, would have sent three follow-up questions and forgotten by Tuesday.

The binder has everything. Accounts at Chase and Schwab. Maggie's pension from the Westport school district. Both life insurance policies. Our wills, drafted by Eileen Brennan in 2019, updated after Sarah's wedding. The estate plan. Login information in a sealed envelope stapled to the inside back cover.

Every Sunday I drive to Hartford to visit my mother Ruth. She's 89. Some days she recognizes me. Some days she asks if I've eaten lunch either way. Arthur kept his finances in his head until he couldn't anymore, and we spent months catching up to reality.

The conversation isn't really about money. It's about making sure the people you love aren't standing in a hospital parking lot at 11 PM — hands shaking, trying to remember the name of your insurance company.

Start with one question. One document. One Saturday morning with coffee.

The binder can wait until next weekend. The conversation can't.