A man I'll call Walter came to one of my Westport workshops in April looking like he hadn't slept in a week. He's 71, retired from a tool-and-die shop in Bridgeport, and he'd just opened a letter from the Treasury Department. It said the government intended to withhold part of his Social Security to collect on a defaulted federal student loan.

Walter never went to college. The loan was a Parent PLUS loan he'd taken out in 2003 to help his daughter finish nursing school. She'd paid him back, more or less. The loan itself, it turned out, never got paid off — and after twenty-two years and a default he'd long forgotten, the government had found him again through the one check he counts on every month.

Let me be direct about this, because the fear in that room was real and a lot of it was unnecessary. Yes, this is happening again in 2026. No, it is not as catastrophic as the letter made it sound. And there is still time — real time — to stop it before a dollar leaves your account. What I told Walter is what I'll tell you.

What's Actually Happening in 2026

For most of the last several years, the government wasn't collecting on defaulted federal student loans at all. Then, on January 16, 2026, the Department of Education announced it was delaying the restart of involuntary collections — including the Treasury Offset Program, which is the mechanism that reaches into Social Security checks — to give borrowers time to move into a new repayment plan. That plan, created under the 2025 tax law and known as RAP, is scheduled to launch July 1, 2026.

Here is the part that matters for your calendar: that delay was a pause, not a cancellation. When the new system comes online around July, the Treasury Offset Program is expected to switch back on. By the government's own estimate, roughly 452,000 Social Security recipients are behind on federal student loans and could see their benefits reduced — and a striking number of them are retirees and people on disability, not the recent graduates most people picture when they hear "student loan."

Why are so many older Americans caught in this? Three reasons I see over and over. Some, like Walter, took out Parent PLUS loans for a child or grandchild — those are federal loans, and the parent is the borrower, full stop. Some carried their own loans for decades through deferments and forbearances that quietly capitalized the interest until the balance was larger than the original loan. And some defaulted years ago, assumed the debt had simply evaporated, and never learned that federal student loans almost never go away on their own. They don't expire. They don't lapse. There is no statute of limitations on federal student debt the way there is on most other kinds. It waits.

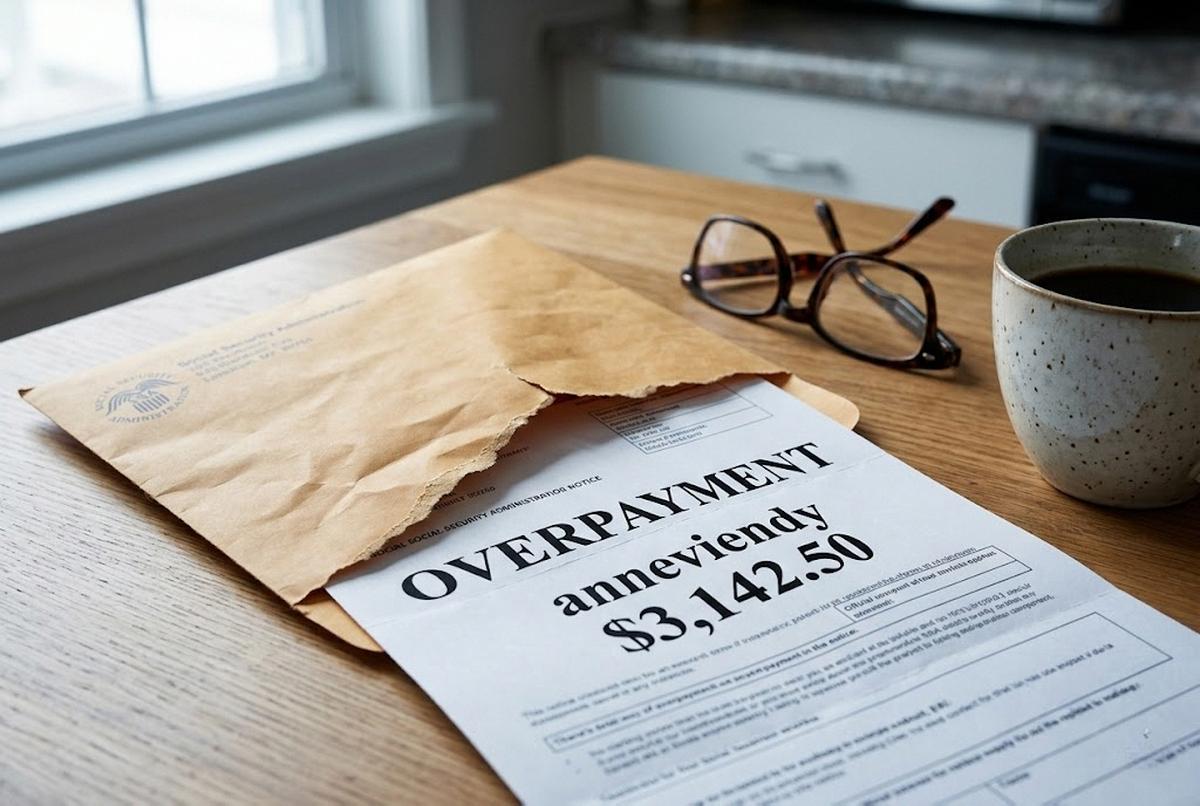

How Much They Can Actually Take

This is where the letters do the most damage, because they're written to alarm you rather than inform you. So let's walk through the actual rule, slowly, because the math is more protective than people assume.

The Treasury can withhold up to 15% of your monthly Social Security benefit to collect a defaulted federal student loan. But there's a floor written into the law: the first $750 a month — $9,000 a year — is fully protected and cannot be touched. More precisely, the offset is the smaller of two numbers: 15% of your monthly benefit, or the amount by which your benefit exceeds $750.

Let me show you what that means with real figures. Say your monthly benefit is $1,600. Fifteen percent of that is $240. The amount above the $750 floor is $850. The government takes the smaller number — so $240 comes out, and you keep $1,360. Now take a more modest check, say $820 a month. Fifteen percent is $123. The amount above $750 is just $70. They take the smaller number again — so only $70 is withheld. And if your entire benefit is $750 or less? They can take nothing. Not a dollar.

I'm not telling you $240 a month is painless. For someone on a fixed income, it's a prescription, a week of groceries, the heating bill in February. But it is a far cry from "they're taking my Social Security," which is the sentence I keep hearing. They are taking a defined slice of the amount above a protected floor — and, as I'm about to explain, only if you do nothing between now and summer.

Who Is Not at Risk at All

Before we get to the action steps, let me clear away some worry that doesn't belong to you. Several groups are simply not exposed to this.

If you receive Supplemental Security Income (SSI), it cannot be offset for student loans — SSI is need-based and fully protected. If you receive Veterans benefits, those are protected too. If your loans are private rather than federal, the Treasury Offset Program doesn't apply to them at all (a private lender would need to sue you and win a court judgment, which is a different and slower process). And if your federal loans are current — in repayment, in an active income-driven plan, in deferment, or in forbearance — you are not in default, and only loans in default get referred for offset. This entire problem belongs to defaulted federal loans and nothing else.

The Ways Out — and Why You Should Move Before July

Here's the good news I led with, now in detail. Default is not a permanent condition. There are four well-established ways out, and every one of them, completed in time, stops the offset before it starts. The window between now and the July restart is exactly when this work pays off.

- Loan rehabilitation. This is usually the cleanest path. You agree to make nine affordable monthly payments over a ten-month period — and "affordable" is the operative word, because the payment is based on your income and can be as low as $5 a month for someone living on Social Security alone. Complete the nine payments and the loan comes out of default, the offset stops, and the record of default is removed from your credit. You generally get one rehabilitation per loan, so do it carefully.

- Loan consolidation. This combines your defaulted loans into a new Direct Consolidation Loan and gets you out of default faster than rehabilitation — often in a matter of weeks — provided you agree to an income-driven repayment plan or make a few qualifying payments first. It's the quicker exit, though unlike rehabilitation it doesn't erase the default notation from your credit history.

- Total and Permanent Disability (TPD) discharge. If you are permanently disabled, this can eliminate the federal loan entirely. This matters enormously for the many people on Social Security Disability caught in this net — in some cases the Social Security Administration's own records can establish eligibility. If you receive SSDI, this is the first door I'd knock on.

- A financial hardship objection. Even as collections resume, you have the right to request that an offset be reduced or stopped by showing that it would cause genuine hardship. This is a slower, less certain route than fixing the default outright, but it exists, and for someone in a tight spot it's worth filing.

The through-line here is simple. Don't wait for the letter to turn into a withholding. Call your loan servicer or the federal Default Resolution Group, find out exactly which loans are in default and what you owe, and start one of these processes now. Rehabilitation in particular takes ten months by design — so the borrower who starts in June is in a very different position than the one who waits until the first reduced check arrives.

If the Offset Has Already Started

Maybe you're reading this after the first reduced deposit already hit. Don't panic, and don't assume it's too late. Starting rehabilitation or consolidation still stops future offsets once the default is resolved. You can request a review of the offset and file a hardship claim. And in certain situations — if you were never properly notified, or you've already been making payments, or you qualify for a discharge — previously offset amounts can sometimes be refunded. Get on the phone with your servicer and document every call: the date, the name of the person you spoke with, and what they told you. In my experience, the paper trail is what protects you.

What I'd Watch, and What I'd Do This Week

I'll be honest about the one thing I can't promise you: the exact timing. This is a policy decision, and policy decisions move. The restart could come precisely in July, or slide a few weeks, or arrive with new wrinkles attached to the RAP rollout. So verify the current status at the source — StudentAid.gov and your own loan servicer — rather than trusting any letter that lands in your mailbox, especially one that pressures you to act through an unfamiliar website or phone number. (Scammers follow these headlines closely, and "resolve your student loan default" is a script they love.)

But here is what I'd do this week if I were Walter. I'd log into StudentAid.gov, or call the Default Resolution Group at 1-800-621-3115, and get a single clear answer to one question: are any of my federal loans in default, and if so, what's the balance? Everything else flows from that answer. If the answer is no, you can stop worrying tonight. If the answer is yes, you've just given yourself a running start on a ten-month clock — and you'll have done it on your terms, not the Treasury's.

Walter went home and made that call. Two of his three loans were already paid; the third, the old PLUS loan, was in default for about $9,800. He started rehabilitation at $12 a month. His Social Security is safe. You've handled harder things than a phone call, and you don't have to handle this one alone.