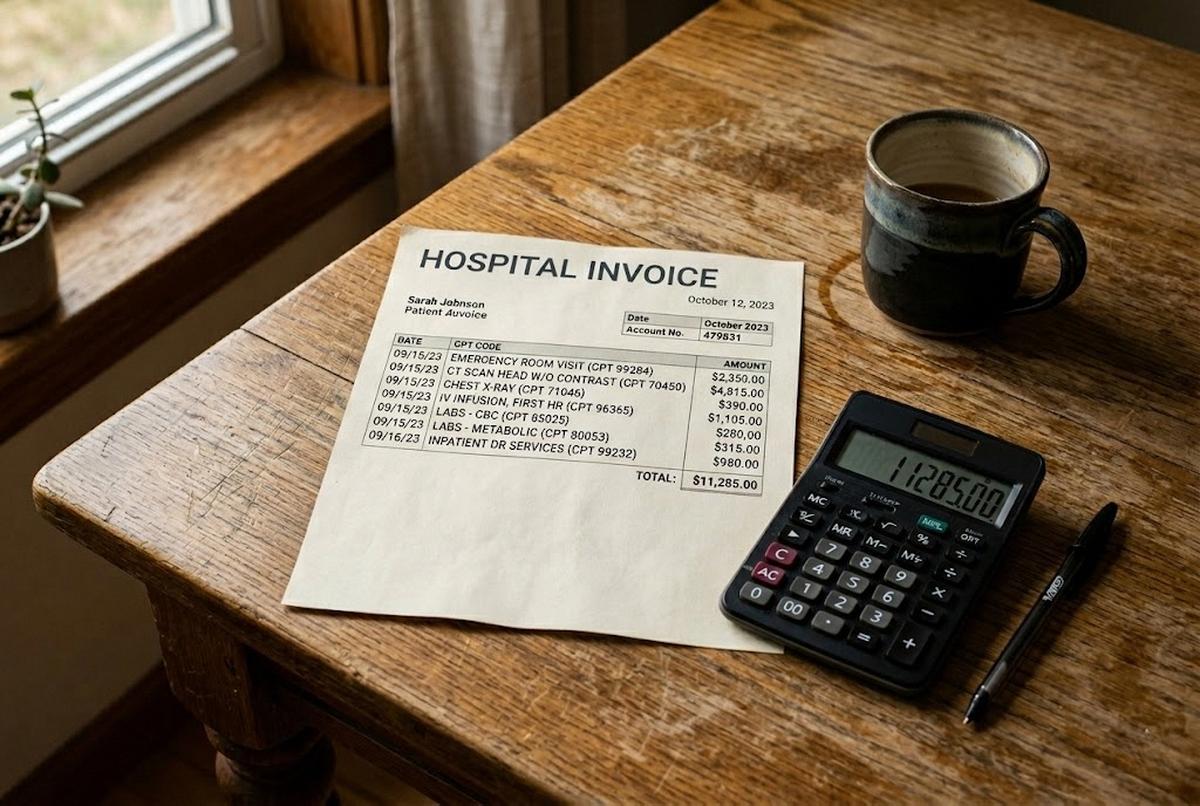

A neighbor of mine, a retired electrician named Russell, handed me a hospital bill last fall for $14,318. He'd had a two-night stay at a hospital in Bridgeport after a fall on his back porch. The summary statement called it "Inpatient Services." That was the entire description. Two nights, $14,318, no breakdown. I asked him to call the hospital and request an itemized bill with CPT codes. The new statement, when it arrived three weeks later, ran 11 pages. The first error I found was on page two: a charge of $487 for a chest X-ray that had been ordered, then cancelled when the doctor changed his mind. The second was a $1,240 charge for a private room. Russell had been in a shared room the entire stay. We were 20 minutes in and we'd already found nearly $1,800 in charges that didn't belong.

This happens constantly. Multiple consumer studies, including reporting from Consumer Reports and analyses from the Patient Advocate Foundation, suggest that somewhere between 30% and 80% of hospital bills contain at least one billing error. The Medical Billing Advocates of America has long cited a figure closer to 80% for hospital bills they audit, though their sample skews toward complex cases. The conservative number from CFPB and FTC consumer reports is roughly 40% of bills contain at least one substantive error, and roughly 40% of patients who challenge a charge get some kind of reduction. Either way, the odds are not in the hospital's favor when a careful person actually reads the bill.

What I want to walk you through here is exactly how to read one. Not the vague "negotiate your medical bills" advice you've seen a thousand times. The specific steps. The federal rules that are now in your favor. The four errors that show up over and over. And the phone scripts that actually work.

The Federal Rules That Are Now on Your Side

Two federal rules matter here, and most patients have no idea either one exists.

The first is the No Surprises Act, which went into effect January 1, 2022, and which the Centers for Medicare & Medicaid Services has continued to refine through 2026. The headline provision: a ban on surprise out-of-network bills for emergency care and for ancillary services (anesthesia, radiology, pathology) at in-network facilities. If you went to an in-network hospital and an out-of-network anesthesiologist showed up in the operating room without your knowledge, you cannot be balance-billed. The hospital has to eat the difference or fight it out with the insurer through the Independent Dispute Resolution process. Read the bill for any out-of-network charge that looks like it shouldn't be there. That's likely a No Surprises Act violation, and the formal complaint process goes through CMS at 1-800-985-3059.

The second rule is the Hospital Price Transparency rule, which took effect January 1, 2021, and was tightened significantly by CMS effective January 1, 2026 (with enforcement starting April 1, 2026). Every hospital is required to post a machine-readable file showing the actual negotiated rates for the 300 most shoppable services, plus a consumer-friendly tool for price estimates. As of the 2026 update, hospitals must now publish median allowed amounts and the 10th and 90th percentile allowed amounts. You can see the real spread between what the hospital charges, what insurers actually pay, and what you might be expected to pay out-of-pocket. The 2026 rule closes a loophole that let hospitals post estimates in vague ranges. They have to post specific dollar amounts now. Penalties for non-compliance run up to $5,500 per day for large hospitals.

And here's the rule almost nobody knows about: under federal billing-rights guidance reinforced by CMS, you have the right to request an itemized bill with CPT codes, ICD-10 codes, and unit counts. The hospital is required to provide it. Your insurer's Explanation of Benefits (EOB) is not an itemized bill. It's a summary. If the hospital sends you a one-page statement that says "Hospital Services: $14,318" and refuses to break it down, that refusal itself is a violation worth escalating. You don't need a lawyer to make this request. You need a phone call and the right phrase.

What an Itemized Bill Actually Looks Like

When the itemized bill arrives, you're going to see a wall of five-character codes next to dollar amounts. These are CPT codes (Current Procedural Terminology), maintained by the American Medical Association. Don't be intimidated. You only need to recognize a few categories.

- Room and board: shown by Revenue Codes on the UB-04 form, not CPT codes. Revenue code 0101 is semi-private room and board; 0110 is private room; 0200-series are ICU/CCU. The accompanying CPT codes you may see (99221–99239) are the physician's daily inpatient evaluation-and-management charges, billed separately from the facility's per-day room fee. A typical Connecticut hospital charges $1,800–$3,500 per night for a semi-private room. Private rooms run $400–$1,000 more per night.

- Lab panels: code 80053 (comprehensive metabolic panel), 80061 (lipid panel), 85025 (complete blood count with differential). These are usually $25–$75 each at the hospital's contracted rate.

- Imaging: 71046 (chest X-ray, two views), 74177 (CT abdomen and pelvis with contrast), 70553 (MRI brain with and without contrast). A chest X-ray runs $300–$700; an MRI can run $2,500–$6,000.

- Emergency department: 99281–99285 (ED visit, low to high complexity). The complexity level is the single most-disputed coding decision on ED bills.

- Pharmacy: usually shown as J-codes (J-codes are HCPCS codes for injectable drugs) or NDC numbers (the 11-digit National Drug Code).

Look up any code you don't recognize at the AMA's free CPT lookup tool or at fairhealthconsumer.org, which lets you see typical charges in your zip code. If a charge runs more than 200% of FAIR Health's typical rate for your area, you have a strong negotiation lever.

The Four Errors You're Most Likely to Find

In 35 years of helping clients sort through medical bills (and lately, neighbors at Ring's End hardware store and people in the pew behind me at Christ & Holy Trinity), these are the four mistakes I see over and over.

1. Duplicate charges. Same lab panel billed twice. Same room night listed on two different lines. The same J-code for the same medication on the same day. Hospitals run charge captures from multiple departments (the lab, the floor nurse, pharmacy), and when systems double-record, nobody catches it because nobody is reading the bill the way you should be reading it. Run your finger down the date column. Anything that appears twice on the same date with the same code needs an explanation.

2. Room dates off by a day. This is the single most common error I see. You were admitted Tuesday afternoon, discharged Thursday morning. That's two nights. The bill shows three. The hospital's billing system charges by calendar day, not by 24-hour period, and discharge-day charges sometimes get added when they shouldn't be. Verify against your discharge paperwork and your own memory.

3. Unbundled lab panels. A comprehensive metabolic panel (CPT 80053) includes 14 individual tests: sodium, potassium, glucose, BUN, creatinine, calcium, the works. The bundled price is usually around $50. Hospitals sometimes "unbundle" the panel and bill each component separately at $15–$30 each, turning a $50 charge into $300+. If you see individual lab tests with codes in the 82000s and 84000s on a day when you also had a panel drawn, that's an unbundling problem. The AMA's coding guidelines explicitly prohibit it.

4. Services not received. This is the one that surprises people most. A medication you refused. A consult from a specialist who walked into the room, said hello, and never came back, billed as a Level 4 consult. A procedure that was scheduled, prepped for, and cancelled. Cross-reference the bill against your discharge summary and your own notes. If you kept any kind of running list during the stay (and I tell every client to do this), pull it out now.

There's a fifth pattern worth knowing about, though it's harder for a layperson to spot: upcoding. That's when the hospital bills for a more complex level of service than was actually provided. A Level 5 ED visit (CPT 99285) when the documentation only supports a Level 3 (CPT 99283). The difference can be $800–$1,500. If you went to the ED for something that resolved in under an hour with a single test, and you see a 99285 on your bill, ask why.

The Phone Calls You're Going to Make

Three calls, in this order. Block out an afternoon. Have the bill, your insurance card, and your discharge paperwork in front of you.

Call 1: The hospital billing department. Not the customer service line. Ask specifically for billing or patient financial services. Get the representative's full name and a direct extension. Open with this: "I'm calling to request a fully itemized bill with CPT codes, ICD-10 codes, and unit counts for my account. I also want to dispute several charges and request a line-item review." If they push back, say: "I understand I have the right to request this under federal billing-rights guidance and the Hospital Price Transparency rule. Please confirm in writing that the itemized bill is being sent." Then list the specific charges you're disputing, by line and date. Document everything. Most hospitals will pause the bill from going to collections during a documented dispute, but you have to ask. Use this exact phrase: "Please place this account in dispute status while the review is pending."

Call 2: Your insurer's claims department. Have the EOB in front of you. Walk through any line where the hospital's bill doesn't match the EOB. Ask: "Why was this service denied?" or "Why was this service paid at out-of-network rates when the facility is in-network?" If the answer involves a coding decision, ask the insurer to file a coding review with the hospital. Insurers have leverage hospitals don't take seriously when an individual patient calls.

Call 3 (only if needed): A patient advocate. Most hospitals employ a patient financial advocate or financial counselor whose job is, in theory, to help you. In practice they're a mixed bag. But they have authority to write off charges, set up payment plans at 0% interest, and apply hospital charity-care policies most patients never hear about. Ask explicitly: "Does this hospital have a financial assistance policy, and what is the income threshold for full or partial write-off?" Nonprofit hospitals are required by IRS rules (specifically Section 501(r) of the tax code) to have a written financial assistance policy and to publicize it. They often don't.

When to Bring in a Professional

If the bill is over $10,000, or if the hospital won't return your calls, or if you're dealing with this on top of grief or recovery, hire a medical billing advocate. The Medical Billing Advocates of America (billadvocates.com) maintains a member directory. Most advocates work on a contingency basis, typically 25–35% of whatever they save you, with no fee if they don't reduce the bill. Some charge hourly at $75–$250. For a $30,000 bill where the advocate finds $9,000 in errors, you'll pay the advocate roughly $2,500–$3,000 and walk away $6,000 ahead.

I tell clients: the math works whenever the bill is large enough that the contingency cut is worth it. For a $4,000 bill, do it yourself. For a $40,000 bill after a hospitalization, get help.

Look for these credentials: Certified Medical Billing Advocate (CMBA), Board Certified Patient Advocate (BCPA), or membership in the Alliance of Claims Assistance Professionals (ACAP). Verify the credential. Anyone can call themselves an advocate.

A Quick Word About Time Limits

Dispute the bill in writing as soon as you spot a problem. The sooner you object, the more leverage you keep — and the easier it is to get an account placed in dispute status before it ever moves toward collections. Once the bill is referred to a collections agency, your leverage drops sharply and your credit can take a hit.

A note on medical-debt credit reporting in 2026: the three major credit bureaus (Equifax, Experian, TransUnion) committed in 2023 to remove paid medical debts and medical debts under $500 from consumer reports, and that voluntary policy is still in effect as of this writing. A separate CFPB final rule (issued January 2025) that would have barred ALL medical debt from credit reports was vacated by a federal court in 2025 and the appeal was dropped. So the bureau policy on small balances remains, but the broader federal rule is no longer in force. Don't count on it as a backstop — dispute fast through the hospital instead.

What to Do This Week

If you've got a hospital bill sitting on the kitchen table right now, or one stuffed in a drawer because you couldn't bear to look at it, here's the order of operations.

- Pull it out. Today.

- Call the hospital and request the fully itemized bill with CPT codes. Use the exact phrase from above.

- While you wait for the itemized bill (allow 7–14 days), pull your EOB from your insurer's portal. Print it.

- When the itemized bill arrives, compare line by line to the EOB. Mark anything that doesn't match.

- Look up unfamiliar CPT codes at fairhealthconsumer.org. Compare charges to typical rates in your zip code.

- Make the three phone calls. Document each one.

- If the bill is large or the hospital is stonewalling, hire an advocate.

Russell got his $14,318 bill knocked down to $9,460. A reduction of $4,858, or roughly 34%. It took him about six hours of work spread over three weeks. He told me later that the hardest part wasn't the phone calls. It was forcing himself to open the envelope.

That's usually the hardest part. Once you've opened it, the rest is just arithmetic and patience. You've handled harder things than this. And you don't have to do it alone. Between the federal rules, the insurer's claims department, and the advocates who do this for a living, there's more help available than you'd guess. Most of it is free. All of it starts with the phone call you've been putting off.

Make the call.

For more on the surrounding decisions families face when a parent's medical costs start adding up, our pieces on how to talk to your parents about their finances, what long-term care insurance actually covers, the new $2,000 Medicare Part D out-of-pocket cap, and the real cost of aging in place all build on the same idea: read the paperwork, ask the questions, and don't pay a dollar more than the rules say you owe.